Djamil Lakhdar-Hamina takes a look at Keynesianism and Modern Monetary Theory and argues they are based on an idealistic notion of science.

“I said, ‘This far you may come and no farther; here is where your proud waves halt!” — Job 38:11 New Living Translation

“Theory, my friend, is grey, but green is the eternal tree of life.” — Lenin, inspired by Goethe

Setting up the terms of the game

What is science? There are two basic answers to this question.

According to neo-positivists, science is the business of coming up with theories, bodies of declarative sentences organized into a deductive system. Some of these statements are couched in theoretical terms, while others are couched in observational terms. Each statement is true if and only if it is verifiable and observable. Therefore, all theoretical statements must be reducible to statements about observations. Ultimately, scientific theories are accepted as the best current theory in virtue of the fact that observable predictions cash out.

According to realists, science is the business of describing and explaining causal mechanisms. Theories are models representing causal mechanisms which explain observable phenomena. Ultimately, we accept or reject a theory if it is true – if it refers to real processes that explain observable phenomena. However, a scientific theory is never final, and we constantly make observable predictions to check the truth of a theory.

In economics, a theory takes the form of a model. The dominant philosophy of science in economics for a long-time was neo-positivism. In the essay “The Methodology of Positive Economics,” Milton Friedman states that a model is accepted because the empirical predictions it made cash out. It does not matter if the assumptions it is based on are true or realistic. What is this unrealistic and idealistic positivism?

The orthodox method in economics assumes a fictitious world of perfect competition, where buyers and sellers have full access to information which makes monopolies absent. The economist then explains reality by how it does not correspond to the fiction. However, in science the theory must best correspond to reality, and if it does not, it cannot claim the label “scientific theory”.

Keynesians and Post-Keynesians are no better because they build a fiction of perfect competition and then add imperfections into the fiction. Apparently, we once lived under “perfect competition” but now reality exhibits “imperfect competition”. Once again, the reality is explained as an imperfection(!), as deviating from the fictitious norm, as opposed to the fiction being way off in the first place. This unrealistic method considers reality imperfect rather than the theoretical quicksand of its own imperfect musings.

This unrealistic method was foreign to Marx who worked to abstract the real features and tendencies of the capitalist mode of production in order to explain its structure and behavior. For instance, he understood how real competition was never perfect and leads, in the long-term, to monopoly. However, there are dynamics and tendencies that act to cohere and break up monopoly power (Sears, after all, is no more). The point is to abstract the real features and tendencies that correspond to reality to come up with an explanatory theory, not to explain reality by how it does not live up to fiction.

The willingness to accept false presuppositions and idealized models is a real scientific faux-pas in economics. In science, it is probably impossible to achieve complete realism. In machine learning, we speak of the trade-off between interpretability and complexity. The more complex (real) a model is, the harder it is to understand and use. Nonetheless, within limits, we strive for maximum realism.

The way I see it, we accept a theory faced with another because it is closer to reality. If the theories make the same predictions it is difficult to determine which to choose. If two competing theories make different predictions, then by observation we can eliminate one. This scientific method allows us to discard theories that we know to be false while keeping theories that do best faced with the evidence.

The history of inflation and unemployment in the 20th century presents the perfect opportunity to test the realism of competing models.

Keynesianism versus Monetarism

Imagine we are in a recession. There is high unemployment, wages are low, and there is little to no growth. We need to stimulate growth and raise employment and wages. We cannot resort right now to socialism.

If you ask most economists, here very loosely monetarists, what would happen if you raise wages?

They look to their models. The model says that the market delivers the real wage and full employment. Hence, messing with the operation of the market will lead you to raise unemployment.

We should observe a rise in unemployment. The best policy then is to not interfere in the workings of the market.

Now if you ask a Post-Keynesian?

They look to the model that has been developed since Keynes (which is very often not the same thing as what the man thought and said). The model says that a market which achieves equilibrium (meaning supply and demand are equal) may not be at full-employment because of depressed effective demand. Increasing wages increases effective demand.

We should observe a fall in unemployment. The best policy then is to increase effective demand through deficit spending.

Which of the two models makes correct predictions? The truth is that both fail to make correct predictions.

There are times when Keynesian theory worked:

- In the era of the Great Depression, the massive deficit spending of the Roosevelt administration was correlated with a return to growth, decreased unemployment, and increased wages. Roosevelt actually tried to stop the level of expenditures in the middle of the 1930s only to witness returning signs of recession.

- A darker example. In 1933, the Nazis engaged in massive deficit spending and other Keynesian measures to pay for rearmament. Within one year of rule they had eliminated unemployment and returned the economy to full employment. Wages were another question…

- In the postwar period, Western governments maintained deficit spending and other Keynesian measures. It surely must have been for something as this was retrospectively dubbed “the Golden age of Capitalism” and saw high rates of growth, low levels of employment, and rising wages in the Western world.

This means there are cases where monetarism’s predictions are worthless. Monetarism cannot explain the recovery, Nazi Germany, and the postwar period. These are significant predictive failings.

However, there are times when Keynesian policy failed.

In the 1958 paper “The Relation Between Unemployment and the Rate of Change of Money Wage Rates in the United Kingdom, 1861–1957,” New Zealand Keynesian economist William Phillips observed a negative correlation, or trade-off, between money wages and inflation. Somehow this trade-off was converted into a trade-off between unemployment and inflation and became encrusted into post-Keynesian orthodoxy; this trade-off is known as the Phillips curve.

In the postwar period, there developed a hubristic belief amongst the technocratic, liberal elite called “fine-tuning.” The belief was that with proper fiscal policy, deficit spending, it was possible to eliminate the business cycle, the volatility of capitalism, and to deliver full employment and robust wages. The trade-off was some inflation, which apparently, with the proper counter-measures, could be tamed.

However, in the 1970s something happened that Keynesian theory had been unable to predict. In fact, post-Keynesians witnessed something that was supposedly theoretically impossible. The 1970s saw stagflation, i.e., rising unemployment and rising inflation. But we were told that with decreasing unemployment came increased inflation and vice-versa! What of the Phillips curve? The Phillips curve broke down. The failure of the Keynesians to predict, explain, and respond to stagflation gave credence to Monetarist economists who at least could claim to have the semblance of an explanation for such a state of affairs. They, therefore, seemed poised to offer a solution.

Therefore, both of these theories have exhibited predictive — and we can surmise explanatory — failings. None of them are able to predict, much less explain, all the cases. Luckily, there is another explanation. It allows us to put the events in their proper place.

Classical-Marxist Explanation

There is a theory that is able to make sense of when Keynesianism worked and when it did not, developed by Anwar Shaikh.1 Shaikh derives his theory from the classical tradition that began with Smith and culminated in Marx.

According to Shaikh, the movements of modern money are shaped by dynamic variables of demand and supply. On the demand side, inflation increases with net injections of purchasing power. It can rise because of government, private, or foreign spending.2

On the supply side, inflation decreases with respect to net profitability, which is profit minus interest and increases with respect to supply resistance, which is the share of profit reinvested. According to Shaikh, the maximum limit of growth is determined by the profit rate at the limit when all profits are allocated to investment.

Intuitively, the decreased net-profitability and increased supply resistance mean there is less space to make a profit through investment in labor and means of production, and tightness on the supply-side puts pressure on capitalists to raise prices. To put it crudely, you can’t produce more, so you raise prices.

The question is always the interaction of these dynamic variables in the observation of an outcome and which is more ‘powerful’ in its effects.

Typically, we observe hyper-inflation in the case when purchasing power increases but the level of output does not.

Stagflation is a case which can be produced when purchasing power increases and net profitability is not as strong as growth, so the tightness on the supply-side translates to increased prices.

A Final Simple Test

But there is an even simpler test to explain the success and failure of Keynesianism. Anwar Shaikh calls it a ‘dividing line’ for Keynesianism. A real limit.

For the cases in which Keynesianism succeeds, net profitability rises faster than wages — the growth of wages is kept in check.

This is precisely the case for the New Deal, as net-profitability regained faster than the rise in wages.

In Nazi Germany, the Nazis financed full employment but took the most scrupulous measures to control prices, wages, and profits. They did not allow wages to sky-rocket, and net-profitability was healthy. Take the following table recreated from the work of Otto Nathan “The Nazi Economic System,”3 which should be taken with a grain of salt, since it was published during the war:

| Annual Average Gainfully Employed | Total Nominal Income | ||||||

| Year | Wage Earners (Millions) | Salaried Employees (Millions) | Total | Wage Earners (Millions of Reichsmarks) | Salaried Employees (Millions of Rms) | Total | |

| 1929 | 14.76 | 3.16 | 17.92 | 23,339 | 7,649 | 30,988 | |

| 1932 | 9.99 | 2.69 | 12.68 | 11,320 | 5,766 | 17,086 | |

| 1933 | 10.89 | 2.79 | 13.68 | 12,051 | 5,722 | 17,773 | |

| 1934 | 12.57 | 2.97 | 15.54 | 14,662 | 6,271 | 20,933 | |

| 1935 | 13.52 | 3.2 | 16.72 | 16,755 | 7,085 | 23,840 | |

| 1936 | 14.35 | 3.46 | 17.81 | 18,752 | 8,064 | 26,816 | |

| 1937 | 15.42 | 3.76 | 19.18 | 21,350 | 8,983 | 30,333 | |

| 1938 | 16.39 | 3.97 | 20.36 | 23,754 | 9,864 | 33,618 | |

| Total Real Income (Corrected to 1929 Prices) | |||||||

| 1929 | 23,339 | 7,649 | 30,988 | ||||

| 1932 | 14,513 | 7,392 | 21,905 | ||||

| 1938 | 28,968 | 12,029 | 40,997 |

Employment and Total Income of Employed Wage and Salary Earners Subject to Social Insurance, 1929-1938

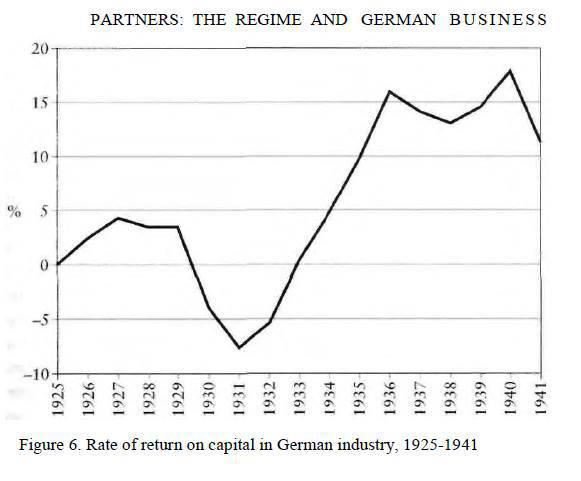

The following is one non-Marxist estimate of the rate of return from Adam Tooze’s, The Wages of Destruction: The Making and Breaking of the Nazi Economy.4 It must serve as a very crude estimate for what we have called “net profitability.”

Using the informal ‘eyeball’ method, we find that the number of employed workers increases but that the wage increase never completely outstrips employment (output was at war-time highs) and is modest in comparison to the explosion in profitability. We, therefore, do not witness inflation.

After World War II, the pattern is reversed, and net-profitability does not sufficiently exceed the growth in wages. We can, therefore, explain the secular rise of the price-level-inflation.

The 1970s saw a collapse in net-profitability while increases in purchasing power through government expenditure and deficit-spending were the case. We can, therefore, expect both unemployment and inflation (i.e. stagflation).

This is obviously a problem for capitalism, as wages are the other side of profit, the drive for producing wealth. Such a situation is simply not sustainable and will in the long-term push the economy towards crisis.

Wrap-up of the game

Post-Keynesianism could not predict certain events, just as Monetarism was unable to give credit where it was due.

Post-Keynesianism was unable to foresee stagflation. They could not even admit its possible existence, and therefore were ill-adjusted to intervene and solve the real problem. This was, in many ways, the trigger for the structural instability of the Keynesian consensus in state and economy.

To simplify a long story, in part because of this failure, people like Milton Friedman were increasingly able to convince the ruling class that theirs was the best theory, primed to solve the problem. Since then, his philosophy has been king in state and economy.

Yet it cannot be denied that Post-Keynesianism was a part of the relative successes of the “Golden Age of Capitalism.” Monetarism would have predicted mass unemployment before the entry of such an economic strategy on the world stage. Instead, there was a recovery from the worst economic crisis in Western capitalism.

A theory is continuously tested by events. In this way, Post-Keynesianism and Monetarism have both been defeated. Why they should still be the only competitors is beyond me. The classical tradition is able to retrodict and put these events in their proper place. The events support the theory better than its competitors.

In brief: I accept the classical theory, its presupposition and models, because they are more realistic than either Post-Keynesianism or Monetarism.

MMT Today

Today, people are desperate to come up with fresh new ideas to rejuvenate a moribund capitalism.

MMT, or Modern Monetary Theory, has come out as a potential elixir.

I cannot do justice to this vast new philosophy, theory, and technology of statecraft and economic policy, but the main MMTers are essentially Post-Keynesians. MMT is now stretching beyond the confines of the academy, and I have heard that people such as Alexanria Ocasio-Cortez see it as a potential financier of the Green New Deal.

One of the main points of MMT is that fiscal and monetary policy should support the goals of full employment and tolerable inflation. In typical Post-Keynesian fashion, recession is explained by deficient effective demand. The level of effective demand can be raised through government deficits and the creation of liquidity. If the economy is exhibiting inflation, the solution is to retract money from circulation.

Of course, MMTers do not claim that inflation, or stagflation, is impossible; in fact, it is a very real possibility for them, but they believe it can be mitigated with fiscal and monetary policy.

Keynes asked of Hayek about his argument in The Road to Serfdom:

I come finally to what is really my only serious criticism of the book. You admit here and there that it is a question of knowing where to draw the line. You agree that the line has to be drawn somewhere (between free-enterprise and planning) and that the logical extreme is not possible. But you give us no guidance whatever as to where to draw it. In a sense this is shirking the practical issue. It is true that you and I would probably draw it in different places. I should guess that according to my ideas you greatly underestimate the practicability of the middle course. But as soon as you admit that the extreme is not possible and that a line has to be drawn, you are, on your own argument, done for since you are trying to persuade us that as soon as one moves an inch in the planned direction you are necessarily launched on the slippery path which will lead you in due course over the precipice.

The truth is that MMT could work, but in the same way, Keynesianism does, within limits.

MMT policy could trigger inflation under a number of conditions.

MMT policy could trigger stagflation if the recovery of net-profitability is not strong enough.

So I ask: When will MMT policy not trigger inflation or stagflation? Where do they draw the line? What are the sustainable limits of MMT?

I am sure MMTers have an answer to such questions, but the onus is on them to explain, in theory and historically, how their measures will not provoke similar consequences to the past. The onus is on them to show the effective limits of their theory and practice.

- I would recommend the reader go through the whole portion part II Turbulent Marco-dynamics to have a deep understanding of Shaikh’s critique of orthodox and Keynesian macroeconomic theory and the construction and testing of his classical macroeconomic theory. Found in Capitalism: Competition, Conflict, Crisis pages. 539-724.

- I owe a large debt for the whole article and this pedagogical presentation of Shaikh’s theory of inflation to Anwar Shaikh’s and Nick Horton’s articles in Socialist Economist found here: http://www.socialisteconomist.com/2018/12/modern-monetary-theory-and-inflation.htmlhttp://www.socialisteconomist.com/2018/05/keynesian-boosts-have-not-always-worked.html

- Ibid , Table 3, page 340

- Ibid , Table 3, page 340

44 Replies to “The Grey Tree of Post-Keynesianism and Monetarism: The Classical Account, Inflation, and Unemployment”

Comments are closed.